In addition to the cost of electricity, the price of hydrogen depends largely on the up-front investment cost of the electrolyzer. The lower the full-load hours, the greater the impact. Analyst BloombergNEF (BNEF) sees a number of different possible pathways for the market to develop.

MARCH 21, 2024

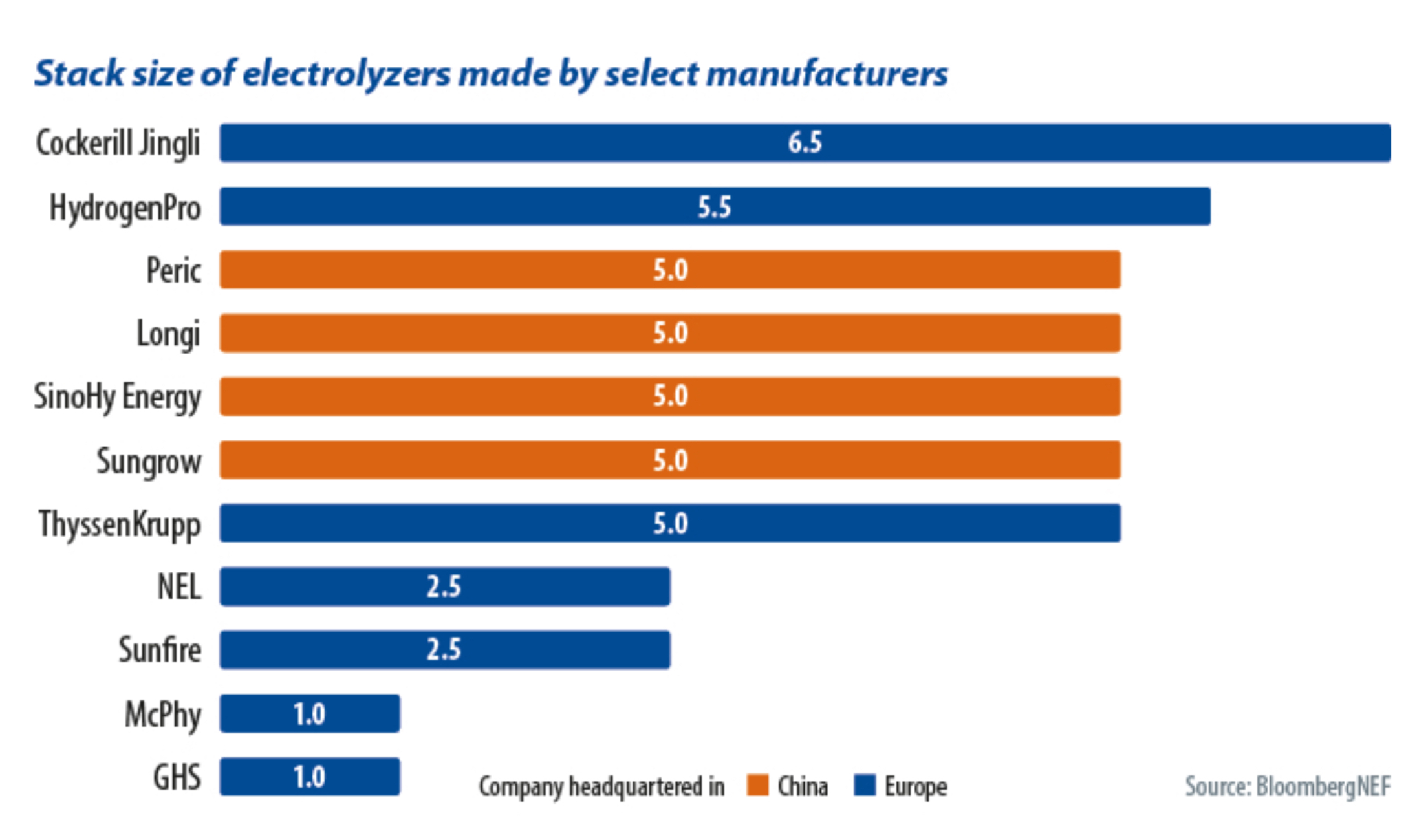

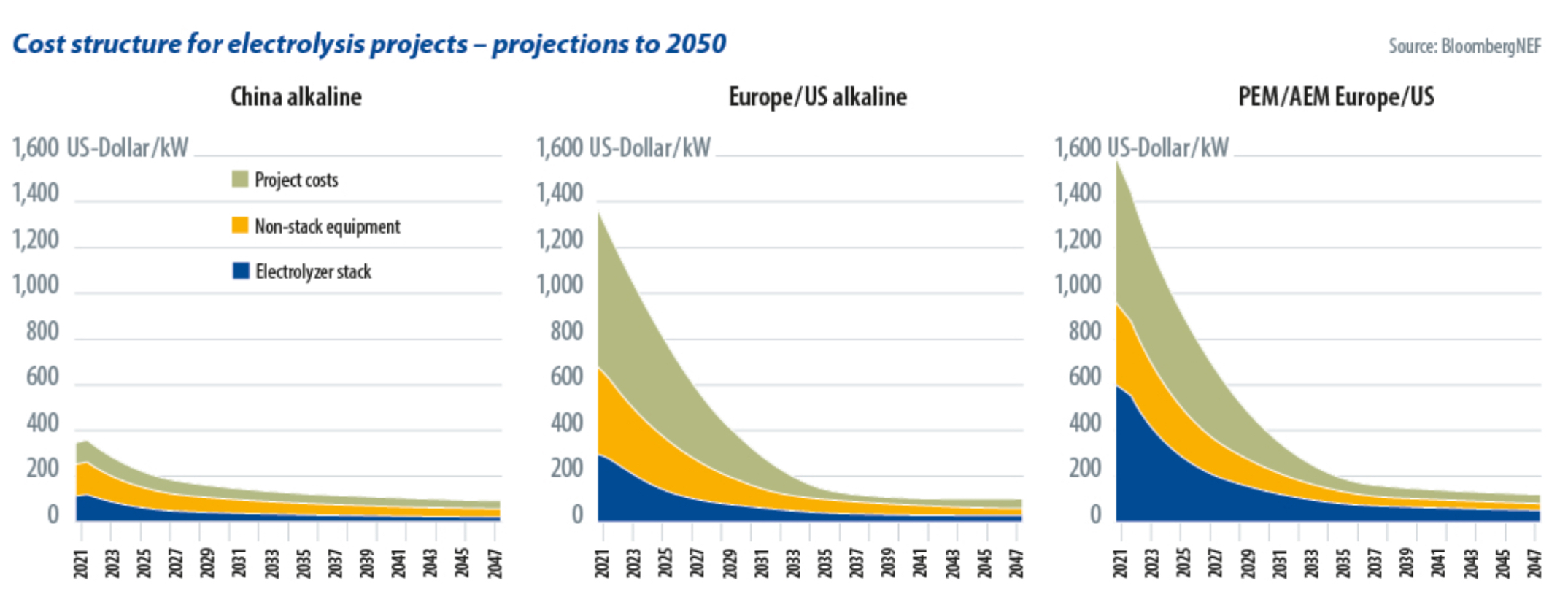

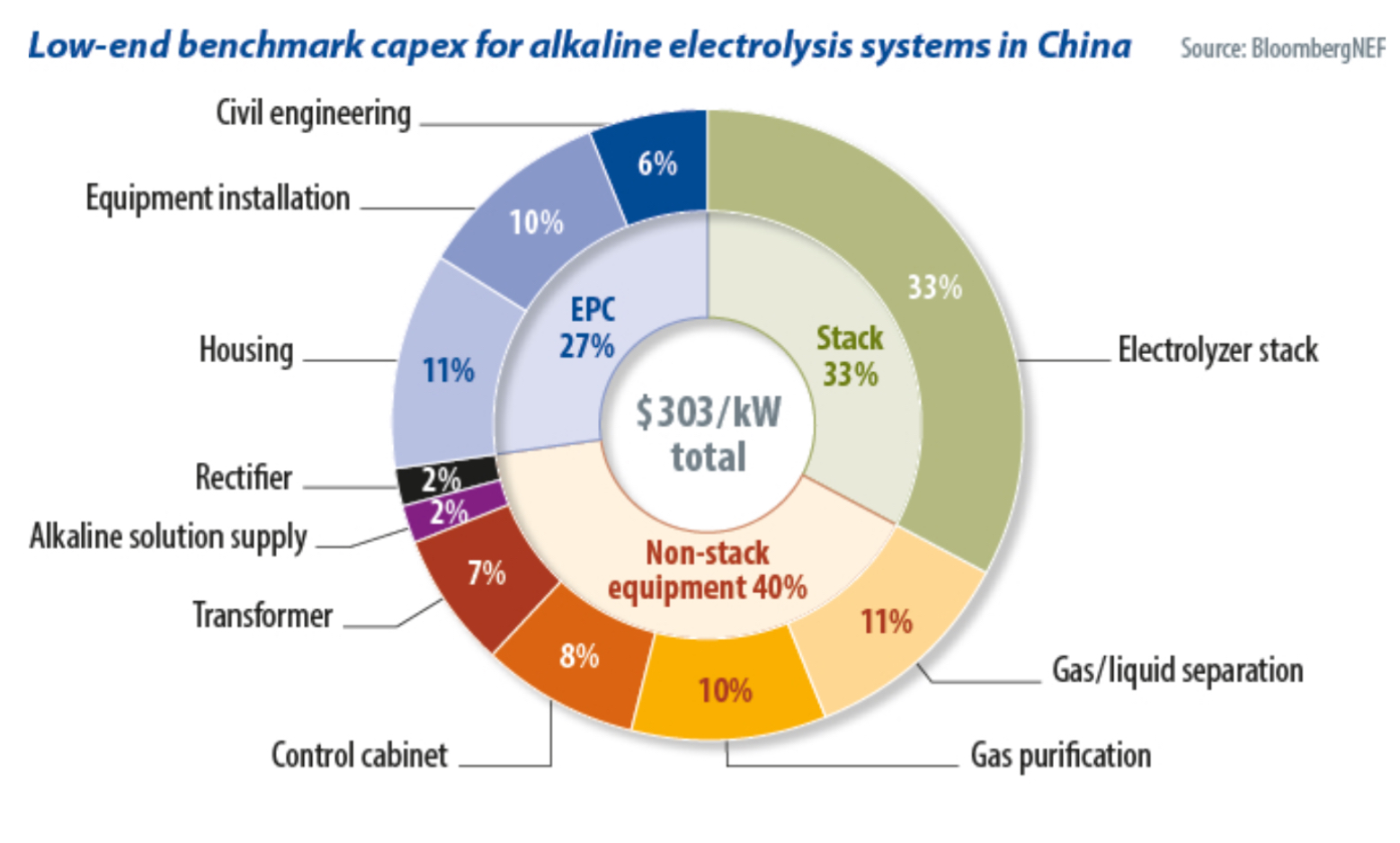

All electrolyzers have a technology-specific stack at their center, in which water is split into hydrogen and oxygen. This consists of carefully layered, gas-tight, welded bipolar plates and plastic membranes – among the main cost factors in every electrolysis plant. Xiaoting Wang, an analyst at BloombergNEF, spoke to 20 companies worldwide as part of the company’s “Electrolysis System Capex [capital expenditure] could drop 30% by 2025” study. This gave her an insight into the cost structure for 30 projects and made it possible to determine the price components for a 10 MW alkaline electrolysis plant in China in 2021, as an example.

The stack accounted for around 33% of the total costs, said Wang, with 40% of the costs coming from the other technical equipment, including power electronics, gas and liquid separation, and gas purification (see chart below). A further 27% of the costs were attributable to other project expense, such as civil engineering, equipment installation, and housing.

Chinese alkaline

The BNEF report stated a 10 MW alkaline system often consists of two stacks of 5 MW that deliver hydrogen at 16 bar. The manufacturer usually offers a complete solution with all accessories and installation. Chinese developers received such an offer in 2021 for as little as $303/kW – that is, a total of around €3 million ($3.2 million). This did not include the grid-connection fee, high-voltage transformers, or other “soft” costs such as expenses for development, approvals and financing agreements.

Wang said that the project costs in Western markets with domestically produced electrolyzers are around four times as high. Investment costs averaged €1,200/kW for alkaline electrolyzers and €1,400/kW for proton exchange membrane (PEM) electrolyzers.

Cheaper offers, such as €180/kW, from Peric for an 80 MW plant in China; or €521/kW, from Thyssenkrupp for a 2 GW plant in Saudi Arabia, do not include all project costs and are, therefore, not comparable. They do include electrolysis stacks, gas liquid separation and purification, and the water supply. However, power electronics and control cabinets are excluded.

Wang attributed this large price difference to low labor costs and the established supply chains in China, where manufacturers of electrolyzers can source materials and components at much lower prices than in the West. Thus far, the production of most electrolyzers is not automated. Chinese manufacturers were producing megawatt-scale electrolyzers for other industries before there was demand from green hydrogen producers, meaning they benefited from scaled production. Existing customers included manufacturers of polysilicon for photovoltaic cells.

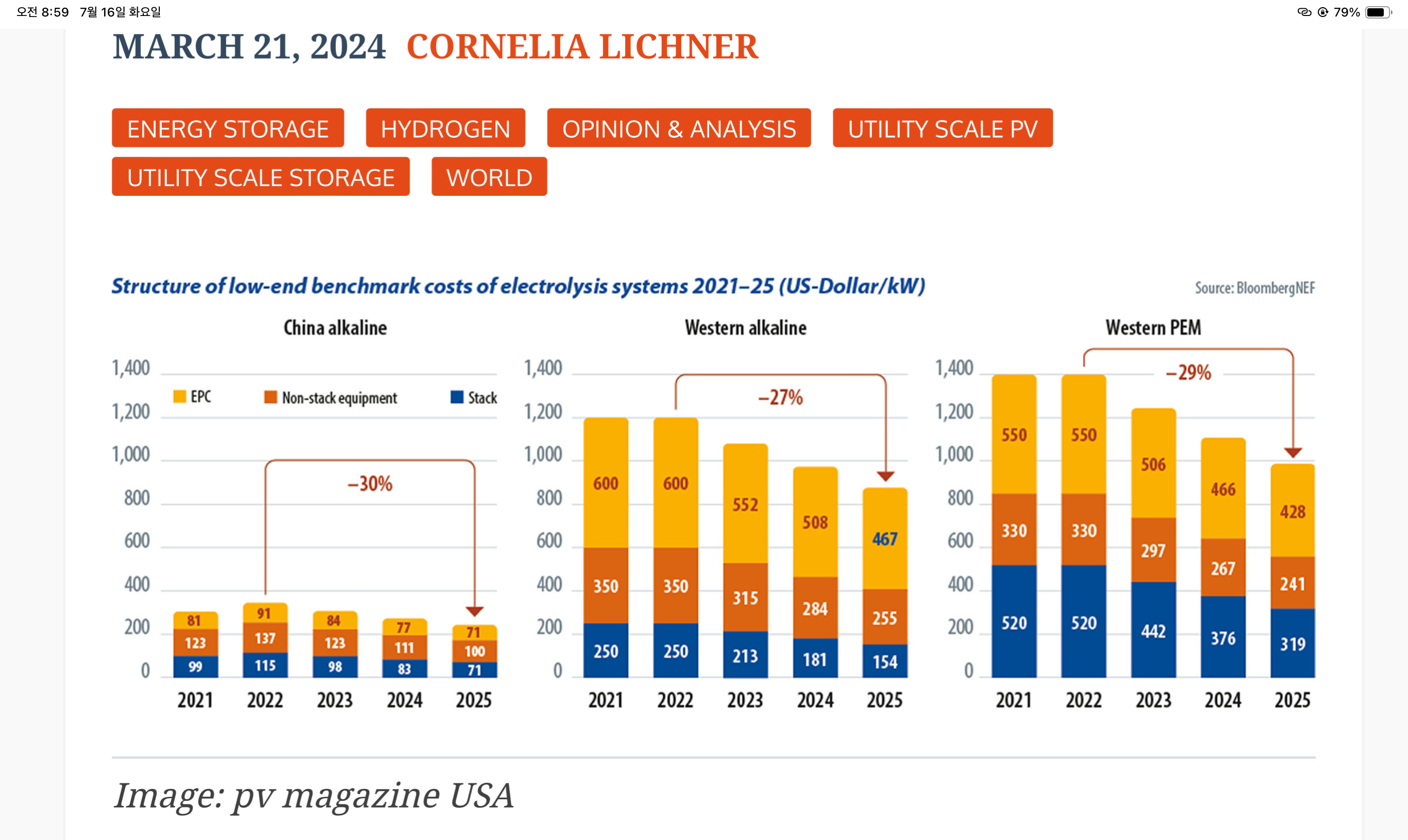

The Bloomberg analysis, from September 2022, claimed that Western manufacturers could achieve similarly low costs. To do so, they would have to utilize highly automated production. Wang said she anticipates significant price reductions by as early as 2025 (see main chart above). Prices for 2021 also still included adequate margins for engineering, procurement, and construction (EPC) companies. Long-term development shows that prices for electrolysis projects will converge worldwide from 2035.

Western investors tend to entrust an EPC company with the handling of an entire project for a lump sum, and to rely on large, well-known companies. Such companies usually have little experience in the construction of electrolysis plants, however, so the safety premiums in the price of the overall offer are high. With increasing experience and the entry of specialized project planners, which leads to more competition, these surcharges should decrease.

Prefabricated containers

Equipment suppliers are also endeavoring to offer products that reduce the workload on the construction site, and thus cut costs. One trend that supports this is the development of containerized systems. This means that the various system components do not have to be assembled on site but are instead prefabricated in a factory, tested, and delivered to the intended location. This minimizes sources of error and reduces the deployment time of specialist personnel on site.

In an update to its market analysis, Bloomberg reported on offers for such container solutions for $1,000/kW. Industry insiders have even reported offers as low as $700/kW, said Wang. One such container solution was presented in a pv magazine Germany webinar in February 2023. The PEM electrolyzer from German supplier H-Tec has an output of 1 MW and produces 450 kg of hydrogen per day. Recordings of pv magazine webinars are available at pv-magazine.com/webinars.

Those who want to reduce costs by purchasing an electrolyzer from China need to consider that exported products are usually sold at a premium of around 20% to 30%, compared to prices on the domestic market, said BloombergNEF, meaning that development and project planning costs would still be higher. It is important to consider that choosing a Chinese brand to supply the core equipment could reduce a project’s chance of receiving local subsidies and could affect financing.

The first green hydrogen projects were, and still are, mainly designed to draw electricity from the grid, with the electrolyzers’ electricity consumption balanced monthly or annually against the suppliers’ renewable electricity generation. In this case, the technical disadvantage of alkaline electrolysis in terms of flexibility would not bother operators.

However, after 2030, most new green hydrogen projects will need to ensure an hourly match between power generation and power consumption for grid-connected electrolysis systems, which will lead to more off-grid projects being developed, said Wang. This trend is not only due to the need for a clearer definition of green hydrogen. A direct connection to renewables generation plants should also improve economic feasibility in the future. After all, using the grid to shift huge amounts of electricity will cost more in the future. Electrolysis with stable grid electricity will, therefore, not be able to produce cheaper hydrogen in the future than with solar and wind energy, with their low electricity generation costs.

Cost reduction

This is where PEM electrolyzers come into play. These can better follow the fluctuating electricity supply and also work efficiently in partial load operation or off-grid. However, this technology still needs to significantly reduce its dependence on expensive platinum group metals, especially iridium, in order to gain a dominant market share, said Wang. Plug Power, from the United States, and ITM Power, from the United Kingdom, use 200 grams to 300 grams of iridium per megawatt of capacity.

Current worldwide production of iridium is around seven metric tons per year. Even if the entire volume were used to produce catalysts for PEM electrolysis, this supply chain could only support a maximum of 35 GW per year. PEM can only dominate the green hydrogen market if manufacturers manage to significantly reduce the consumption of iridium per unit this decade or achieve an equivalent effect in parallel with improved metal recycling. Wang said Electric Hydrogen, a new United States-based manufacturer of PEM electrolyzers, has already reported using significantly less iridium than competitors.

There is also a chance that anion exchange membrane (AEM) electrolysis could replace PEM after 2030 because it does not use expensive metals. This means manufacturers must succeed in developing stacks that are suitable for large scale projects. Enapter is an AEM pioneer, building small stacks and assembling them into larger 1 MW units which are still small compared to other electrolyzers. California-based company Verdagy is just starting to sell 20 MW modules, each consisting of two 10 MW stacks.

More competition

The costs of Western products could initially fall by around 30% by 2025. In addition to technological progress, competition is also likely to increase. Manufacturers worldwide have announced a production capacity of 52.6 GW for this year while deliveries are optimistically only 5 GW, according to BloombergNEF’s forecast. In China, where there is already fierce competition for orders from project developers, manufacturers’ margins are small. In addition, developers hedge their risk against the manufacturer by paying only up to 85% of the agreed price on delivery and the rest once commissioning has been completed and performance is still good after 18 months.

The pressure is not yet as high on Western markets, as investors and project developers in Europe and the United States can reckon with relatively high subsidies. However, production capacities are also increasing here and factories need to be fully utilized. If Chinese manufacturers also seek their salvation in exports, it is foreseeable that the price war will increase in all markets.

Yanmar and Amogy have entered into a Memorandum of Understanding (MoU) to integrate Amogy’s advanced ammonia-cracking technology into Yanmar’s hydrogen internal combustion engine (H2ICE). This collaboration seeks to pioneer a solution for decarbonising marine power generation.

The partnership will focus on combining Amogy’s technology with Yanmar’s H2ICE to provide low-cost hydrogen fuel. Amogy’s ammonia-cracking technology uses catalyst materials to break down ammonia into hydrogen and nitrogen at lower reaction temperatures with high durability, minimising heating and maintenance requirements. This integration promises a comprehensive clean energy solution for decarbonising marine power generation.

Furthermore, building on this joint research, both companies will explore the potential for collaboration in developing maritime hydrogen fuel cell systems.

“We are excited to work with Amogy on this innovative project,” said Ken Kawabe, Group Leader at Yanmar Research and Development Centre. “Our commitment to a sustainable future aligns perfectly with this collaboration, and we believe that integrating Amogy’s ammonia-cracking technology with our H2ICE has immense potential for decarbonising marine power.”

“As pioneers in sustainable energy solutions, we are thrilled to collaborate with Yanmar in exploring the integration of our cutting-edge ammonia-cracking technology with their hydrogen internal combustion engines,” said Seonghoon Woo, CEO at Amogy. “Collaboration is critical to advancing clean energy solutions and, together, we can overcome challenges and expedite sustainable progress in the marine sector.”

The collaboration between Amogy and Yanmar began in 2023 when Yanmar Ventures, Yanmar's corporate venture capital arm, invested in Amogy. Since then, both companies have been exploring opportunities to integrate their technologies.

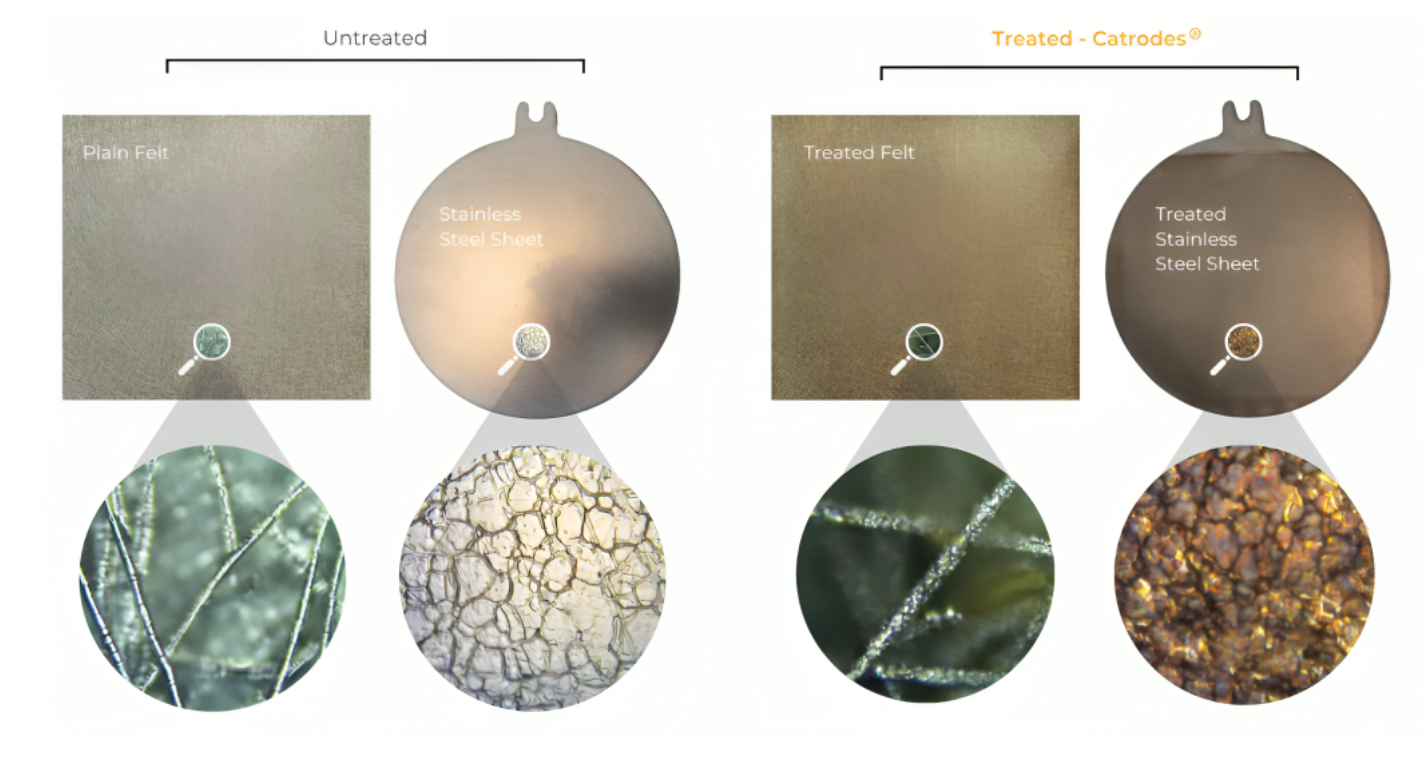

PGM-free Electrodes for AEM and Alkaline Electrolysis - Catrode®

With Latent Drives' innovative electrochemical treatment process, they activate stainless steel electrodes to make Catrodes® which combine both catalyst and electrode as one homogeneous part, without additional ingredients. Catrodes are PGM-free (Platinum Group Metal) robust high-performance products. The production process is developed for high volume mass production at realistic costs – reducing the capital costs of Green Hydrogen. The Catrode is a Ni-Fe catalyst. First, the electrochemical surface area is increased then chromium is removed, and nickel is migrated and exposed on the surface of the stainless steel felt to produce a nickel iron catalytic surface layer. The catalyst layer is formed on stainless steel felt which acts as both the Catalyst, Electrode and Gas diffusion layer combined. Catrodes are 0.6mm thick with an active area of 200 cm² as standard but different thickness and areas could be treated as a custom request. PGM free Catrodes performance in OER is comparable with state-of-the-art precious metal catalysts such as platinum and iridium and significantly surpasses the performance of nickel electrodes at a much-reduced cost. Catrodes exhibit a stable performance below 1.58V RHE at 0.2A/cm2 at 50°C for 22 hours run in an ElyFlow test cell with an active area of 10 cm² compared to the overpotential of a commercially available Catalysed Nickel foam which reached 1.69V RHE. The PGM-free Electrodes are designed to be run wet i.e. with liquid electrolyte in contact with the Catrode and membrane. Not intended for use with Nafion membranes. Key features

Suitable for AEM and Alkaline Electrolysis PGM-free (Platinum Group Metal) robust high-performance products Developed for high volume mass production at realistic costs Catrode is a Ni-Fe catalyst Available in different thickness and areas as a custom request Comparable with metal catalysts such as platinum and iridium and significantly surpasses the performance of nickel electrodes at a much-reduced cost PGM-free Electrodes for AEM and Alkaline Electrolysis - Catrode®_2

Application areas

For alkaline water electrolysis, with either AEM or Zero Gap designs. For use with Potassium Hydroxide (KOH) electrolyte in concentrations from 01.M to 5M. Catrodes were developed to be used as anodes but can also be used as cathodes in an alkaline electrolyser. Catrodes may also have potential to be used in batteries and fuel cell technology but after mutual collabaration with Latent Drive. Use cases

Catrodes are being used as the combined gas diffusion layer and catalyst in a European electrolyser startup. Catrodes in the form of treated stainless steel sheet is also being developed for a customer. Contact us

Latent Drive is at the forefront of fuel cell technology innovation for novel applications. Interested? Please contact the vendor by filling in the contact vendor form.